Mental Models discussed in this podcast:

- Normal Distribution (Statistics)

- Resulting (Read: Annie Duke’s book)

- Efficient Market Hypothesis

Please review and rate the podcast

If you enjoyed this podcast and found it helpful, please consider leaving me a rating and review. Your feedback helps me to improve the podcast and grow the show’s audience.

Follow me on Twitter and YouTube

Twitter Handle: @TreyHenninger

YouTube Channel: DIY Investing

Support the Podcast on Patreon

This is a podcast supported by listeners like you. If you’d like to support this podcast and help me to continue creating great investing content, please consider becoming a Patron at DIYInvesting.org/Patron.

You can find out more information by listening to episode 11 of this podcast.

Show Outline

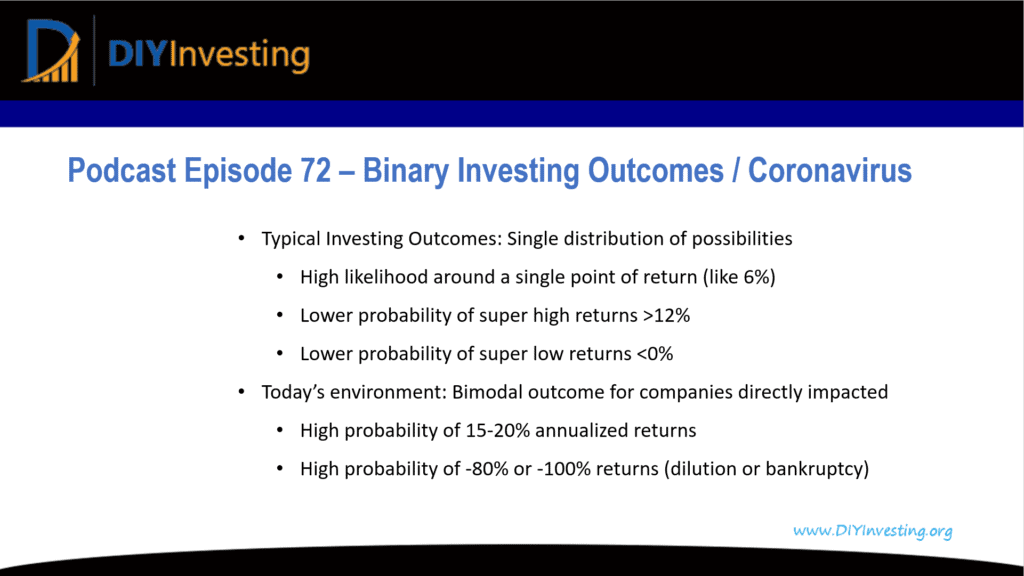

How coronavirus has modified the distribution of investment returns

- Typical investing outcomes – single distribution of possibilities

- High likelihood of a single point of returns (say 6%)

- Low probability of super high returns (>12%)

- Low probability of super-low returns (<0%)

- Today’s environment has a bimodal outcome for many companies directly impacted by the coronavirus shutdown.

- Instead of a single point of high probability outcomes, we have two center points. (15% and -80%)

- One may be around 15-20% annualized returns, but the other is highly negative and bounded by the zero-based outcome of the bankruptcy of the company.

- “The market has priced it in.”

- It is almost impossible for the market to accurately price in a bimodal distribution of potential returns.

Summary:

Investors today are likely underestimating the potential for bankruptcy of their favorite companies. Regardless of the long-term return of underlying assets, bankruptcy is possible when debt covenants are breached or a negative liquidity event occurs.

Both are possible outcomes in today’s investing environment as most companies are not well situated for handling a long period of zero revenues. (Not zero profits, but zero revenues)