Mental Models discussed in this podcast:

- Leverage

- Fractional Reserve Banking

- Margin

- Economies of Scale

- Operating Leverage

Please review and rate the podcast

If you enjoyed this podcast and found it helpful, please consider leaving me a rating and review. Your feedback helps me to improve the podcast and grow the show’s audience.

Follow me on Twitter and YouTube

Twitter Handle: @TreyHenninger

YouTube Channel: DIY Investing

Support the Podcast on Patreon

This is a podcast supported by listeners like you. If you’d like to support this podcast and help me to continue creating great investing content, please consider becoming a Patron at DIYInvesting.org/Patron.

You can find out more information by listening to episode 11 of this podcast.

Show Outline

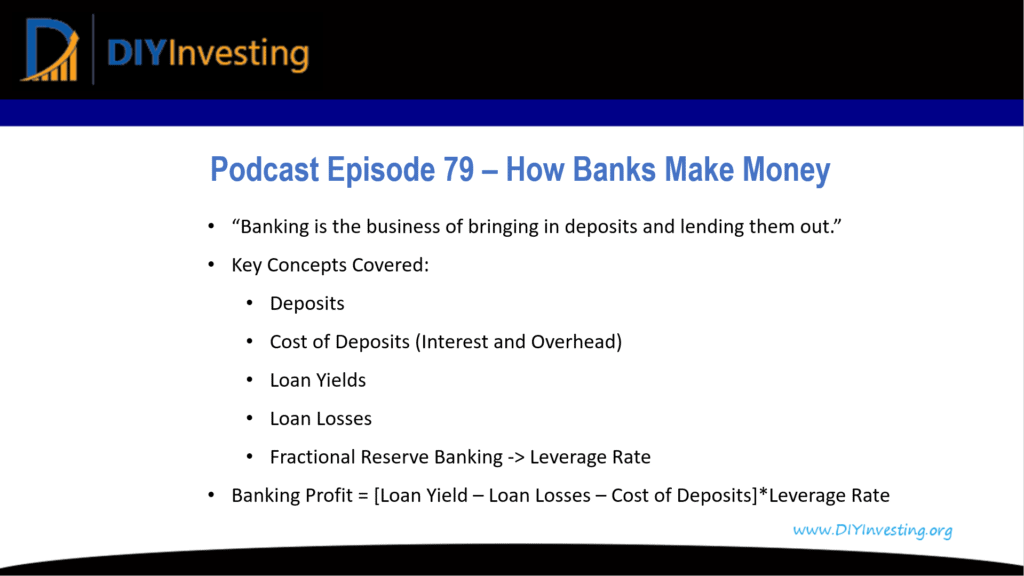

Banking Business Model – Key Concepts

As some of you may remember, one of my goals for this year is to improve my understanding of bank stocks. Today’s podcast will focus on the basic business model that banks use to make money.

Key Concepts:

- Deposits

- Cost of Deposits

- Direct Cost: Interest Rates paid on Deposits

- Indirect Cost: Overhead (Employees, Rent, etc…)

- Loan Yields

- Loan Losses

- Fractional Reserve Banking -> Leverage Rate

- ROE = ROA * Leverage

- Banking Profits = Loan Yields – Loan Losses – Cost of Deposits – Overhead

A recent movie I enjoyed about Banking

- Recently watched: The Banker on Apple TV+

- Two black entrepreneurs in the 1960s buy two Texas banks.

- Samuel L. Jackson

- Anthony Mackie

The movie follows their journey and the ensuing blowback by Jim Crow.

One of the things the movie did very well was to explain the basic banking business model. Banks are easiest to understand when you focus on single branch banks instead of large money center banks like JP Morgan or Wells Fargo.

Summary:

Banking is the business of bringing in deposits and lending them out.

Banking is a perfect example of a capital intensive business. A bank cannot grow unless it receives capital in the form of deposits. Deposits are the lifeblood of a bank and only through healthy deposit growth can a bank sustainably grow loans and therefore profits.