The NACCO Industries spin-off occurred in September 2017. You can find the investor presentation I am reviewing on NACCO’s website through this link. The presentation is dated September 18th, 2017.

NACCO Industries, Inc (NYSE: NC) spin-off of Hamilton Beach Brands (NYSE: HBB) September 2017 Investor Presentation Review

In August of 2017, a NACCO Industries spin-off of their Hamilton Beach Brands subsidiary was announced. Then, in September NACCO published this investor presentation to help investors better understand the spin-off. Theoretically, this would allow you to decide whether you wanted to continue owning both companies, only one of the companies, or neither. For my sake, I am examining this investor presentation after the NACCO Industries spin-off has occurred. Spin-off presentations can be particularly useful for learning about the business model of a company. These are my notes and thoughts while reviewing this presentation.

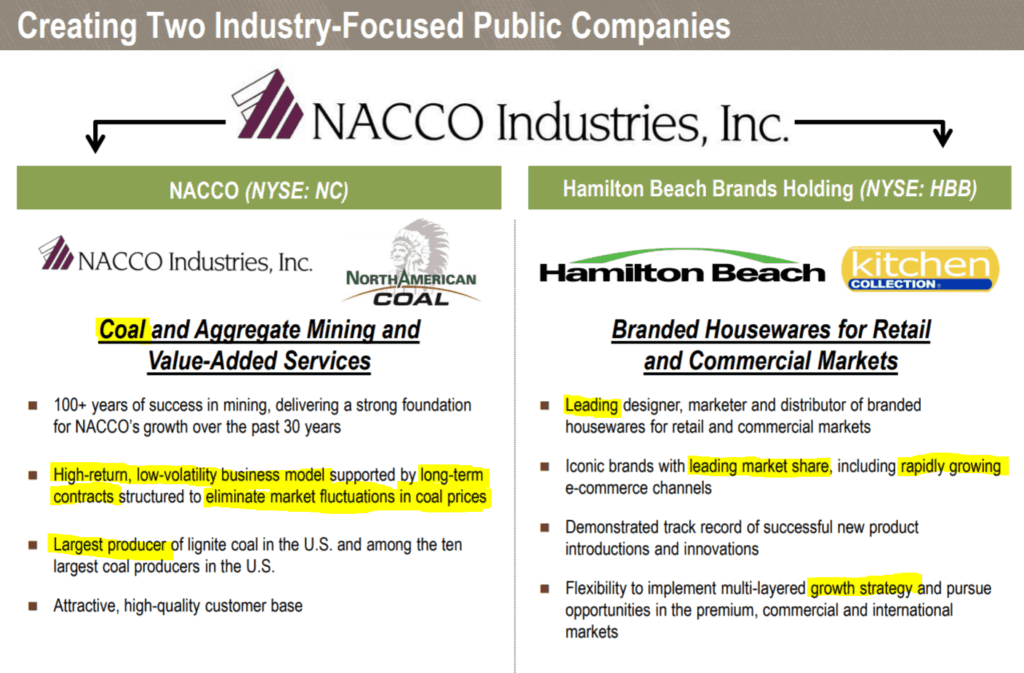

Slide 3 – NACCO Industries Spin-Off

The two companies are operating in completely different industries. NACCO operates in the coal and aggregate mining industries. Meanwhile, the Hamilton Beach Brands company is a consumer discretionary company selling home goods. These two companies would have zero synergies. It makes sense that they would be separate companies.

A few keywords leap out at me on this slide. “High-return, low volatility business model” and “long-term contracts structured to eliminate market fluctuations in coal prices.” This is interesting. I need to find out more information on the ability to eliminate coal price exposure.

NACCO also has a long history and is the market share leader in their market.

Keywords I notice regarding Hamilton Beach Brands: “leading market share” and “rapidly growing.” So, while NACCO is low-volatility, Hamilton Beach Brands seems to be a growth play.

Slide 4 – Reasons for the NACCO Industries spin-off of Hamilton Beach Brands

This slide confirms my thought from slide 3. These companies would best operate separately. Management provides their reasons for the NACCO Industries spin-off on this slide.

Slide 5 – NACCO Executive Succession

There is no real turnover in NACCO’s executive leadership.

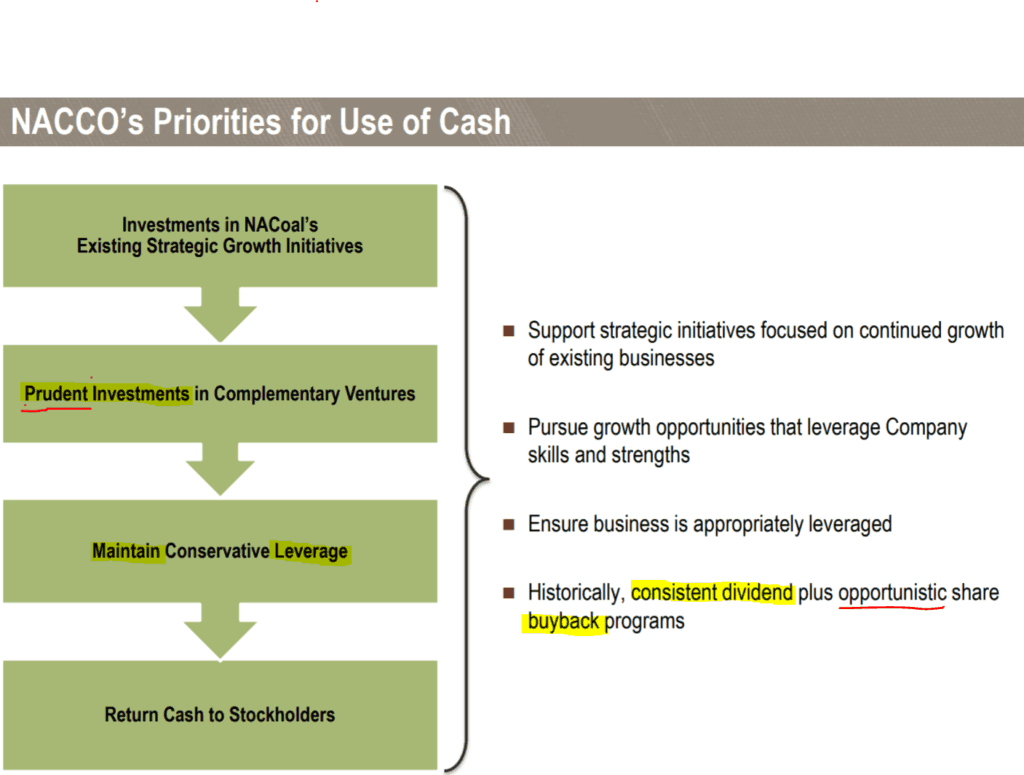

Slide 6 – Future Capital Allocation of NACCO Industries spin-off

Capital allocation is one of the most important responsibilities of management. Therefore, I paid close attention to this slide. NACCO plans to use cash for four purposes: grow current businesses, grow new business, maintain leverage, and return cash to stockholders.

I like the emphasis on “prudent investments.” While further research would be required, it’s nice to know that management won’t plan to grow simply for growth’s sake.

Maintain leverage means that they believe current levels of debt are ideal. Therefore, I shouldn’t expect large debt increases and I also shouldn’t expect debt to be paid off. This last point is particularly relevant. When a company pays off debt with cash, they are unable to return that cash to shareholders. You’d prefer to not own companies while they are actively paying off debt because it’s less lucrative to you as an investor. This is a positive sign.

Management plans to return cash to shareholders. Although this is the last priority for management, at least it’s one of the four priorities. Most importantly is the focus on, “consistent dividends” and “opportunistic share buyback programs.” Consistent dividends are good for investors. Dividends are a proven form of return on investment. Consistent dividends also help prevent management from wasting cash. My favorite part of the whole slide is the opportunistic nature of the buybacks. Share buybacks are a popular form of returning to cash to shareholders. However, they can be value destructive if executed at high prices. The focus on only opportunistic share buybacks means that management understands this fact.

Slide 8 – North American Coal (NACoal) Business Model Overview

NACoal’s business model consists of surface mining of coal for power generation.

NACCO is a service business with “cost-plus contracts.” The cost-plus contracts are what eliminate the coal price fluctuations. That’s good to know. It answers my question from earlier.

I should do more research on mine-mouth operations. The keyword “exclusive supplier” means NACCO doesn’t face competition here.

There are some things you just like reading in a potential investment. “Steady income and cash flow with minimal capital investment” has to be near the top of the list. Who doesn’t like that?

Learning about the business model is important. The entire goal of fundamental analysis is to focus on the business, not the stock.

Slide 10/11 – NACoal’s Safety and Environmental record

NACoal appears to have the best safety record of all coal producers. They also seem to have a good environmental record. That’s good. A positive safety and environmental record should reduce lawsuit and regulatory risk.

Slide 12 – The location of NACoal’s facilities across the United States

NACoal’s facilities are diversified across six states.

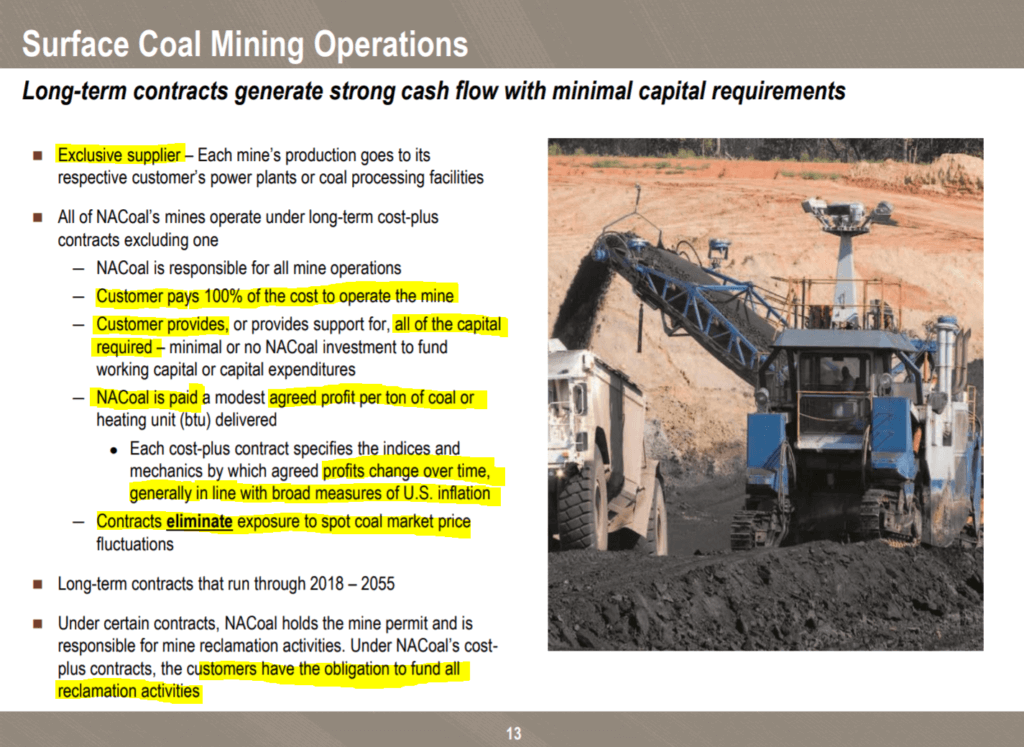

Slide 13 – NACCO Unconsolidated Coal Mining Business Model

The cost-plus contracts are long-term. However, one of their mines doesn’t have the same contract setup as the rest.

Contract structure:

- NACCO’s customer pays 100% of the costs to operate the mine. This is basically a form of synthetic equity for NACCO Shareholders. Synthetic equity is a form of leverage.

- Minimal investment from NACoal is needed in the form of capital expenditures or working capital.

- NACCO/NACoal is paid a fixed profit per ton or BTU delivered to the customer.

- The agreed upon profits are inflation adjusted.

- NACCO’s profits have zero exposure to the spot coal price.

Slide 14 – NACCO’s Consolidated Mine

Mississippi Lignite Mining Company (MLMC) operates under a different contract. NACCO is actually responsible for the costs and liabilities of this mine. This makes MLMC less beneficial than the other mines. However, they do have a long-term sales contract with a customer to be an exclusive supplier.

Slide 15 – Coal Mining Operations results for 2016 by location

The three largest mine contracts expire between 2035-2045. Those three mines produce 25.5 tons of coal. The company as a whole produced a total of 32.5 tons. Therefore, these three mines represent 78% of the business. Assuming the power companies stay in business, these mines should be productive for at least 17 years.

Slide 16 – North American Mining (NAM) subsidiary

There is potential growth in the lime rock business.

Slide 18 – NACCO Strategy

NACCO wants to grow by applying their cost-plus model to other industries. They have been successful in growing production by adding new locations over the last 7 years. However, the future might not be as bright.

Slides 19/20 – NACoal’s production growth since 2012

NACCO Industries’ coal production has grown in recent years. New locations have driven a large part of the increase.

Slide 23 – NACCO Financial Summary

I need to do further analysis of the cash flows shown. It appears that pre-tax income is about $16 million for the first six months of 2017. If the business isn’t cyclical, then that would mean $32 million in annual profit for 2017. However, I expect it’s a cyclical business because they are fueling power plants. Electricity usage varies by season, so I would assume power plant output does as well. I need to investigate further.

Total debt is $69.1 million. Cash is $54.9 million. However, NACCO will receive $35 million from Hamilton Beach Brands prior to the spin-off. Consequently, the company should have positive net-cash after the spin-off. The net cash position allows us to value the company solely on cash flows.

Slide 24 – NACCO Industries’ Competitive advantages post spin-off

The power plants of NACCO’s customers are apparently more efficient than coal power plants which have closed recently. This warrants further investigation into what causes coal power plant closures.

Slide 27 – Risk Factors Appendix

NACCO has a lot of apparent risks as a coal company.

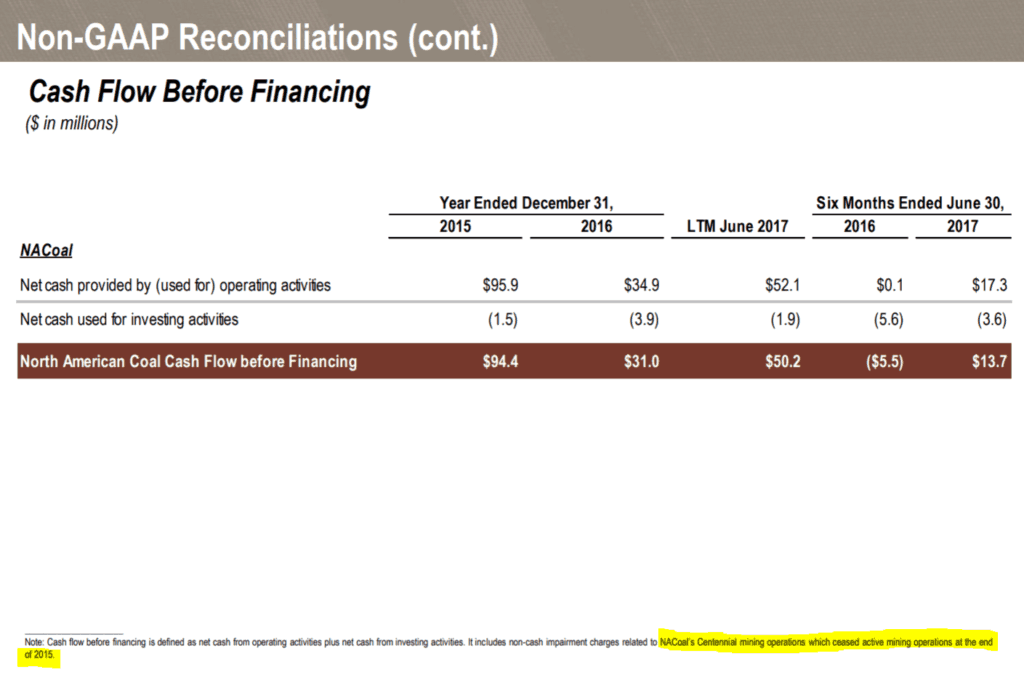

Slides 30/31 – Non-GAAP Earnings reconciliations Appendix

What is Centennial?

Slide 32 – Cash Flow Appendix

Cash flow appears to be higher than I thought from Slide 23. Are cash flows possibly as high as $50 million per year? 2015 even lists cash flows of $94 million. However, there is a note at the bottom that discusses why this might not be the case.

In particular, it appears that Centennial was a mine which operating previously but ceased mining operations in 2015. Although the mine is closed, apparently NACCO still has liabilities related to that mine.

Fundamental Analysis Examples Live

In order to increase both my posting frequency and regularity, I am trying something new on a trial basis. I often read company’s annual reports, 10K, 8K, quarterly earnings reports, and conference call transcripts. Every once in a while, I’ll review an investor presentation made by a company’s management. During that process, I take notes and write down my thoughts about the company and what I’ve learned. I hope to increase the value I am providing readers by publishing my notes publicly.

The length and polish of these posts will be different than other work on this site. I expect that my average post of this type will be much shorter than some of my theory based posts. As I am trying to share my process, the notes are likely to be more stream of consciousness writing. For example, they could be quite short if I don’t have much to learn or add from a particular earnings report.

Starting this week, I will be publishing notes from my personal fundamental analysis work. If anyone has any feedback on whether seeing my process in action is valuable, please post that in the comments. I’m also open to comments about how I can improve. I’m always trying to get better at providing value to you the reader.